Collections become an infrastructure problem at platform scale

Platforms invest heavily in making loan approvals faster, onboarding smoother, and payouts instant. But what truly determines the long term health of a lending business is not how quickly money goes out.

It is how reliably it comes back in.

At small scale, repayment tracking feels manageable. A few reminders. Manual matching. Spreadsheet oversight. Teams can monitor incoming transfers and reconcile them without too much strain.

Then growth accelerates.

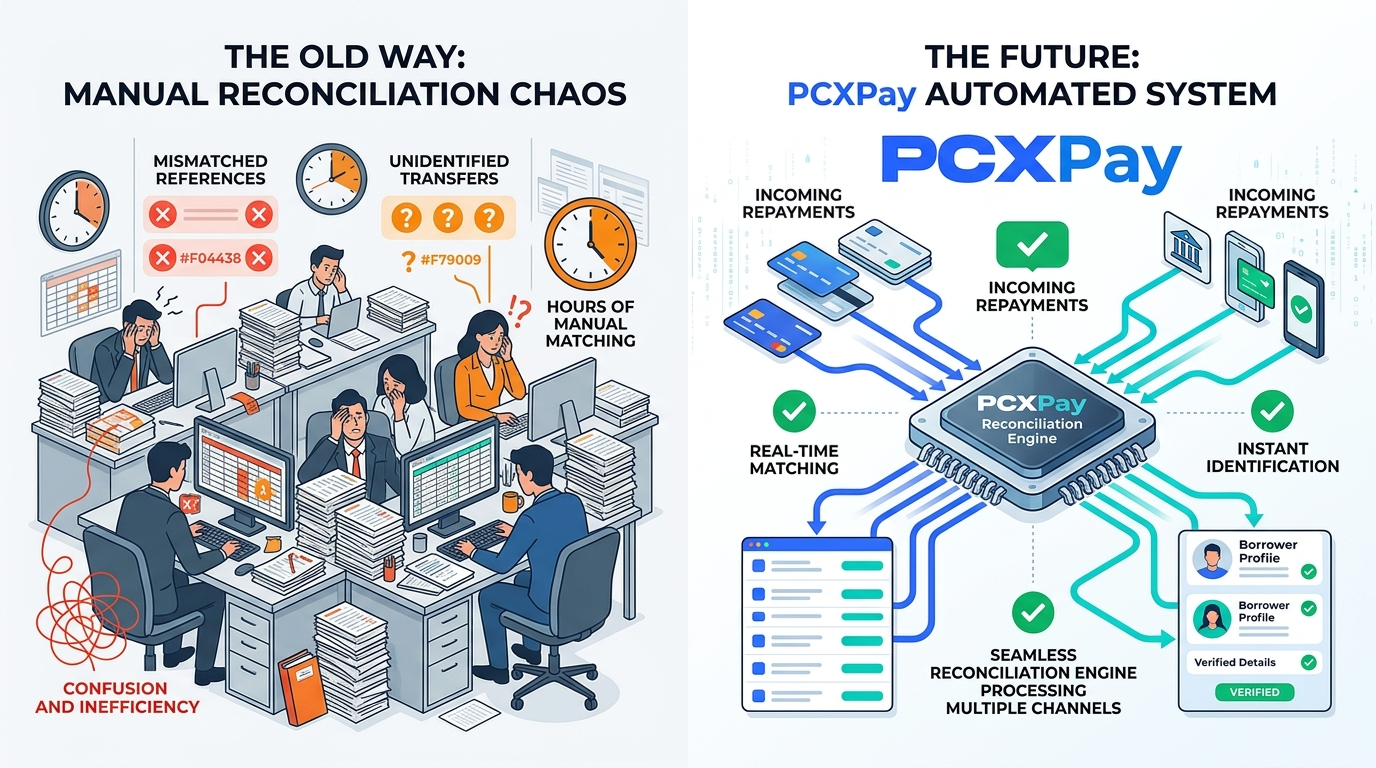

Hundreds or thousands of borrowers begin repaying across different banks, channels, and currencies. Payment references are inconsistent. Some repayments arrive late. Others arrive without clear identifiers. Reconciliation becomes time consuming and error prone.

Liquidity planning becomes uncertain.

When Collections Become a Liquidity Risk

Unpredictable repayments create operational instability.

Treasury teams cannot confidently forecast inflows.

New loan disbursements are delayed due to cash flow uncertainty.

Investor reporting becomes reactive instead of structured.

Staff spend hours manually tracking and matching payments.

Borrowers who attempt to repay but do not see confirmation quickly begin to question the system. Support requests increase. Trust weakens.

The real risk is not missed payments alone.

It is unpredictability.

Embedded finance platforms do not fail because they cannot lend. They struggle when they cannot reliably collect.

Why Collections Must Be Infrastructure Driven

Automated loan collection is not just about sending reminders. It is about connecting repayment channels directly into reconciliation, settlement, and treasury systems.

At PCXPay, automated loan collection rails integrate repayment methods into a coordinated backend infrastructure. Incoming payments are automatically identified, matched in real time, and reflected instantly within platform systems.

This means:

Repayments are linked to the correct borrower immediately

Balances update without manual intervention

Treasury dashboards reflect accurate inflows

Liquidity forecasting becomes structured

Collections move from reactive chasing to predictable financial management.

The Operational and Strategic Impact

Consider a growing lending platform expanding across multiple regions. Without automated infrastructure, each new market introduces additional repayment complexity.

With PCXPay, collections scale without multiplying manual processes. Liquidity becomes visible. Disbursements can be scheduled confidently. Investors gain confidence in the platform’s financial stability.

Borrowers benefit as well. When repayments are acknowledged instantly and balances reflect accurately, trust strengthens. The repayment experience feels clear and controlled.

Liquidity is not sustained by disbursement speed alone. It is sustained by repayment predictability.

At PCXPay, automated collection infrastructure transforms loan repayments into structured cash flow. That predictability supports growth, protects liquidity, and builds long term stability in embedded finance platforms.