Mobile Money Is Not a Single Rail: Understanding the Fragmentation Across Africa

The Illusion of Uniformity

It is easy to assume that if one mobile money integration works in one country, it will work everywhere else. The reality is more complex.

MTN in Ghana operates differently from MTN in Nigeria. Safaricom’s M-Pesa has its own architecture, regulatory framework, and settlement behavior.

These are not variations of the same rail. They are entirely different systems that happen to share a similar user experience.

Each one comes with its own API behavior, failure modes, reconciliation logic, and compliance requirements. Treating them as interchangeable leads to brittle integrations and inconsistent user outcomes.

Where the Real Complexity Lives

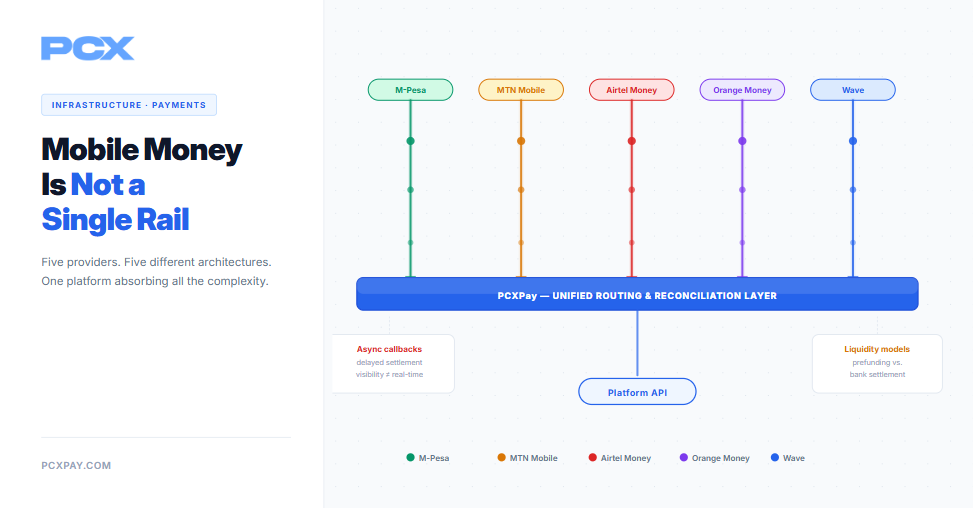

The complexity is not at the interface level. It sits deeper in the infrastructure.

Transaction confirmation is not always real time. Some providers operate on asynchronous callbacks that may delay final settlement visibility. Others require polling mechanisms or manual reconciliation fallbacks.

Liquidity management also varies. In some markets, wallet prefunding is required. In others, settlement depends on banking partner availability. This directly impacts whether a transaction can be completed instantly or must wait.

Regulatory expectations differ as well. KYC thresholds, transaction limits, and reporting requirements are not standardized. What passes compliance in one country may be rejected in another.

For engineering teams, this means a single “mobile money integration” is actually a collection of country-specific systems that must be handled independently, even if abstracted at the product layer.

Why This Breaks at Scale

At low volume, these differences can be managed manually. Teams monitor transactions, handle exceptions, and reconcile inconsistencies in the background.

At scale, that approach collapses.

Failed callbacks, delayed settlements, and mismatched transaction states begin to accumulate. Support tickets increase. Finance teams lose visibility. Engineering teams spend more time debugging edge cases than building product features.

What looked like one rail becomes multiple operational risks.

Designing for Fragmentation

Reliable mobile money infrastructure starts with accepting that fragmentation is permanent.

At PCXPay, mobile money is treated as a set of distinct rails connected through a unified routing and reconciliation layer. Each provider is integrated with awareness of its specific behavior, not abstracted away blindly.

This allows transactions to be routed intelligently, retries to be handled based on provider characteristics, and settlement to be tracked with clarity across markets.

The goal is not to simplify the underlying systems. It is to absorb their complexity so that platforms do not have to manage it directly.

If your platform is expanding across African markets, the question is not whether you support mobile money. It is whether your infrastructure understands how different each “mobile money” rail actually is.

Learn how PCXPay unifies fragmented payment rails into a single, reliable infrastructure layer for African markets.