Stop Guessing Who Sent You Money: How PCXPay Virtual Accounts Make Reconciliation Effortless

Then, the friction begins.

Suddenly, you have hundreds of users sending identical amounts with incomplete or differently formatted references. What once took minutes now consumes hours of operational time. At this stage, reconciliation quietly shifts from a background process to a massive growth bottleneck, stalling the very momentum you worked so hard to build.

The Structural Failure of Shared Collection

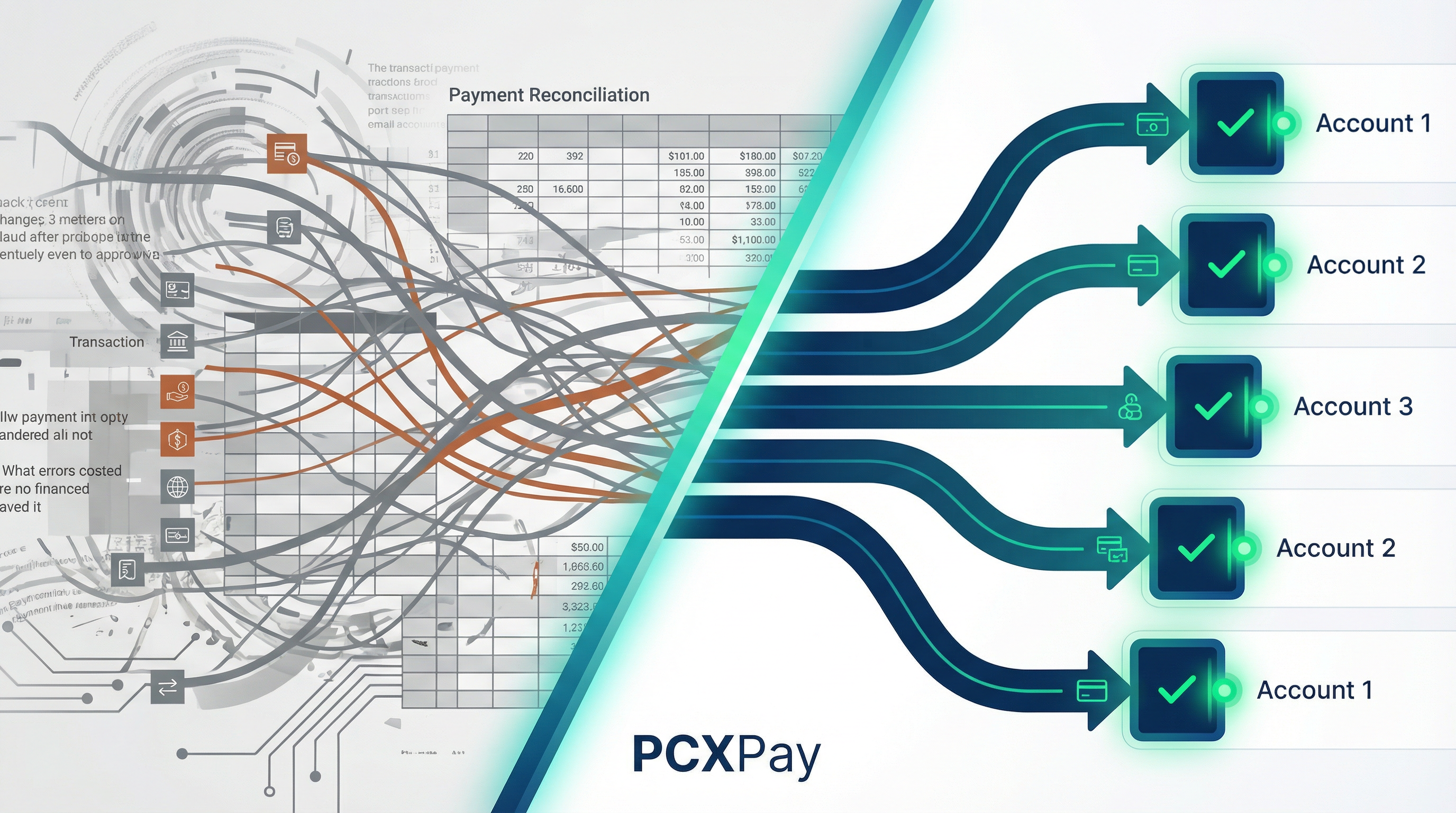

The fundamental flaw of shared accounts is that identification happens after the money arrives. This forces finance teams to reverse-engineer ownership, triggering “spreadsheet fatigue” and an immense operational strain. When transactions are matched manually, confirmations lag, support tickets surge, and your background processes become a daily burden.

As you expand across regions, this friction only compounds. For the user, every delay creates uncertainty: Did my payment go through? Why is it not reflected? When identification isn’t instant, trust …the most expensive currency in fintech begins to erode.

Moving from Manual Matching to Infrastructure-Led Growth

Reconciliation is an infrastructure decision, not an accounting function. If your system doesn’t identify payments at the source, growth only multiplies friction. We built PCXPay Virtual Accounts to solve this at the root.

Programmatic Assignment. By assigning unique account numbers via our API, every inflow is automatically linked to the correct ledger the moment it hits. Real-time Webhooks. Instant notifications alert your system the second a payment is successful, triggering value delivery without manual intervention. Granular Ledger Control. Even with incorrect amounts, the system identifies the sender instantly, ensuring exception handling remains an automated process rather than a manual investigation.

At PCXPay, virtual accounts integrate directly into your settlement and reporting systems. Whether you are managing ten or ten thousand repayments, every transaction is recorded instantly regardless of whether the user included a reference.

Start Scaling with Confidence. When you stop guessing who sent the money, your back office finally keeps pace with your front-end ambition.

Ready to automate? speak with our solutions team about integrating dedicated virtual accounts today.