Why Embedded Finance Becomes Expensive Faster Than Platforms Expect

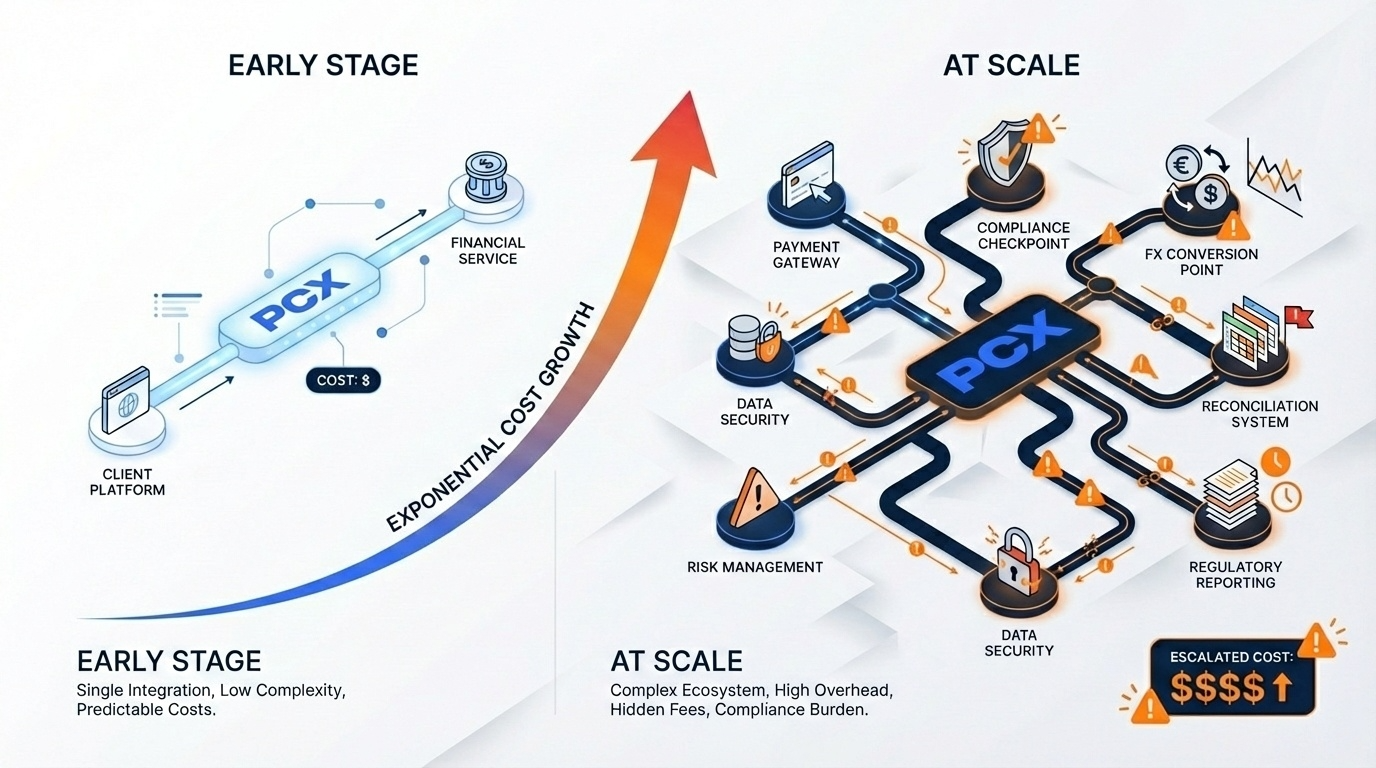

The Hidden Costs Behind Growth

Many platforms underestimate the operational burden of handling finance at scale. Payment failures require investigation. Reconciliation becomes complex. Compliance demands constant attention. Small inefficiencies compound over time.

What starts as a feature quickly turns into an infrastructure challenge.

Teams that were focused on product development find themselves managing financial edge cases. Engineering resources are diverted to maintain payment flows instead of improving user experience. Costs rise, often quietly.

Why Infrastructure First Thinking Matters

The difference between sustainable growth and constant firefighting is infrastructure design.

Platforms that treat finance as infrastructure early build systems that can absorb complexity without exposing it to users. They rely on specialized providers to handle routing, settlement, FX, and compliance, instead of reinventing these systems internally.

At PCXPay, our role is to absorb this complexity at the infrastructure layer, so platforms do not carry the full operational cost as they scale.

Designing for the Long Term

Embedded finance works best when it is predictable, reliable, and largely invisible. Users do not want to think about payments. Platforms do not want to manage financial plumbing.

When finance is designed as infrastructure rather than a feature, costs become more controlled. Growth becomes more sustainable. Teams can focus on what actually differentiates their product.

The real question is not whether platforms should embed finance. It is whether they are prepared for what comes next.

Infrastructure makes that difference.