Why Embedded Finance Platforms Cannot Rely on a Single Payment Rail

The Illusion of Simplicity

A single rail feels efficient because it reduces integration work. Fewer partners. Fewer contracts. Fewer dashboards.

But payment rails are not static systems. They experience downtime. They change pricing. They introduce new compliance rules. They limit corridor coverage. They slow down under volume pressure.

When everything depends on one rail, a single failure becomes a platform wide disruption.

For users, this shows up as failed transactions.

For finance teams, it shows up as reconciliation stress.

For leadership, it shows up as revenue volatility.

At scale, concentration risk becomes infrastructure risk.

Why This Becomes Expensive

Imagine a lending platform operating across three countries. If its only payout rail experiences delays in one region, borrower disbursements stall. Collections slow. Liquidity planning becomes uncertain.

Or consider a marketplace expanding internationally. One rail may support domestic transfers well but struggle with cross border settlement. Growth becomes constrained by infrastructure limitations rather than market demand.

The cost is not just downtime.

It is missed expansion.

It is lost trust.

It is operational instability.

The Infrastructure Reality

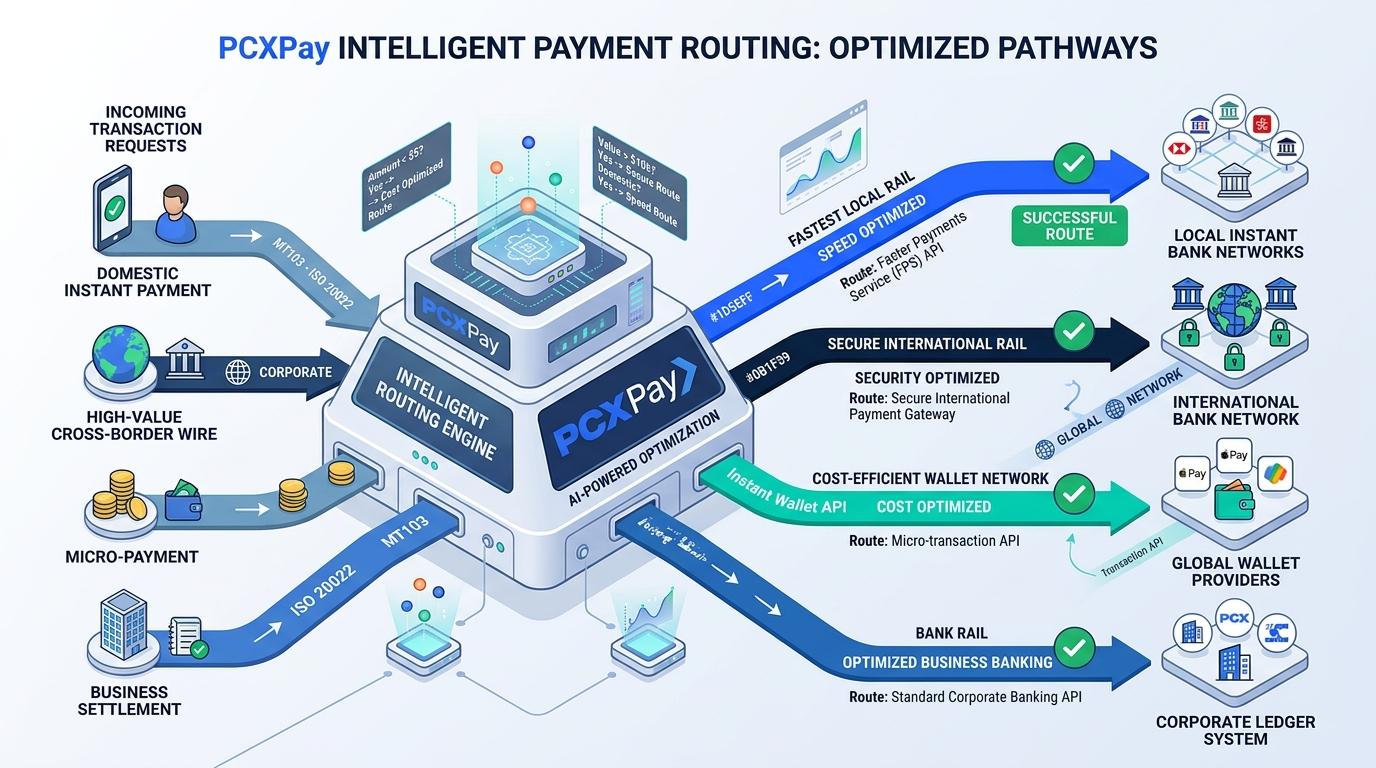

No single payment rail performs optimally across all corridors, currencies, and transaction types.

Domestic instant payments differ from cross border wires.

Wallet transfers differ from bank settlement flows.

High value transactions differ from micro payments.

Each rail has strengths and weaknesses.

At PCXPay, we treat payment rails as components within a broader infrastructure strategy. Rather than forcing platforms into one route, we build connective layers that intelligently coordinate across multiple rails.

This reduces dependency risk.

It increases routing flexibility.

It protects growth.

What This Enables

When platforms operate with diversified payment rails:

They maintain uptime even if one provider faces disruption.

They optimize routing for cost and speed.

They expand into new markets without rebuilding from scratch.

They protect their users from backend instability.

Users never think about rails.

They only notice when payments fail.

Embedded finance infrastructure should not rely on a single path. It should be resilient by design.

At scale, redundancy is not complexity. It is stability.

And stability is what sustains growth.